Revisiting the outlook

The health of the Australian construction sector remains a key area of focus for both equity and credit investors. In this report, we take a timely review of the sector outlook, noting the recent trends in costs, profitability and the degree of financial distress.

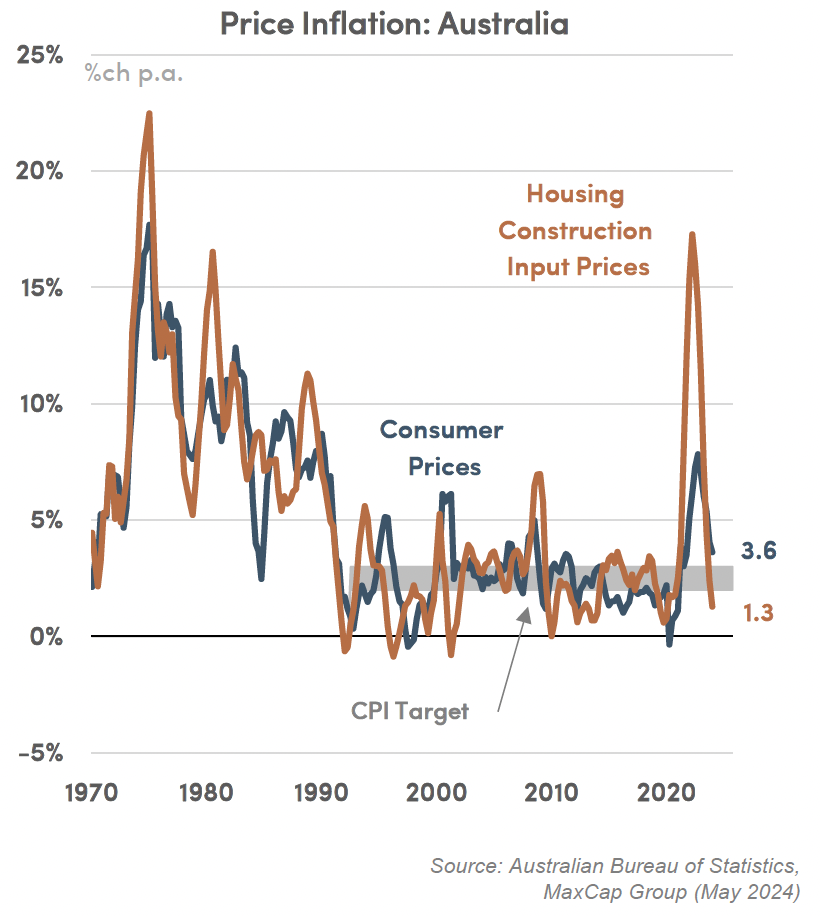

Past peak inflation

The worst price shock since the 1970s looks to be behind us, as construction cost inflation slows sharply. Building costs are finding their peak and may fall outright. This is only a partial unwind, but it does provide much-needed relief for stressed builders.

Sunnier days ahead

Indeed, the adverse profit drivers of recent years are now unwinding, particularly as construction costs stabilise, final selling prices rise, interest rates approach a cyclical peak, and we move back to sunnier weather in the more populated parts of Australia.

A more profitable vintage

In this context, we are expecting a distinctive shift in construction profitability, as builders move on from the loss-making projects from 2022, into what is shaping up to be a progressively more profitable set of projects in 2024 and beyond.

Diminishing builder distress

Meanwhile, the profit squeeze of recent years has driven more builders into insolvency. As these profit drivers improve, we expect construction insolvencies to slowly decline from here, even in the face of a broader economic slowdown in 2024.

Implication for investors

From a credit perspective, there is still a lot of work to do, even as cyclical conditions improve, to keep an eagle eye on builder / developer performance, particularly in terms of their cost management, project profitability and capacity for loan servicing.