Staying alive

After a tumultuous 2023, global real estate investors are bracing for more difficult conditions in 2024, perhaps this is best summed up by the industry catch cry of “stay alive ‘til ’25” to illustrate the challenges of high interest rates, lower values and rising distress.

Survive and thrive

In this context, investors are looking more broadly for demand growth and resilient returns, leading many to the relatively stable and less correlated markets of Australia and New Zealand, where firm population gains are driving an unfolding surge in demand.

The big pivots

With interest rates holding higher for longer, passive and levered real estate strategies reliant on cheap debt no longer work. Indeed, investors are keenly reallocating from passive to active, from office / retail to living / logistics and from equity to credit.

“We have strong conviction in living and logistics, especially in more fragmented sub-markets, where we can find value, strong fundamentals, severe undersupply and downside protection via hybrid capital structures.”

Head of Equity Investment

Seeking shelter

Changing demand and falling prices are locking in underperformance for specific sectors for years ahead. Passive rent collection is challenging. Levered beta is strained by elevated rates. Instead, look to firmer sectors, alpha generation and resilient credit.

Life in the fast lane

Undoubtedly, residential is shaping up as the standout sector for the year ahead, given rapid population growth, alongside diminished supply, driving marked undersupply. Already, housing markets are responding with broad gains in rents and values.

Tips for navigating 2024

Given this market outlook, our three pieces of advice for the year ahead are… seek shelter (from underperforming sectors), take more credit (to improve portfolio returns) and live a little (and track the robust drivers for residential and other living sectors).

The credit compass points to Australia

In a world with elevated interest rates, the case for real estate credit is looking more compelling, supported in Australia by firm population gains, robust housing demand, higher funding costs and good structural resilience.

From brain drain to brain gain

In an unpredictable and volatile world, Australia remains an open island of stability, increasingly drawing larger volumes of immigrants – particularly the young and the highly educated – which provides a welcome boost to economic demand, at a time of challenging demographic headwinds elsewhere.

More resilient real estate markets

Australian real estate asset prices are structurally more resilient, demonstrated over 40 years of history and again in this global downturn. Importantly, milder asset price swings domestically help to moderate credit investment risks.

Vital lending market features

There are key structural market features that work for the lender in Australia. Full recourse loans mean borrowers cannot simply ‘hand back the keys’ and ‘walk away’, typically resulting in low instances of credit default and losses.

The tailwinds are not this strong everywhere

Altogether, Australia stands out well relative to other developed credit markets, given very different degrees of market resilience. The sharp market distress currently unfolding in Europe and the US looks more muted here.

Australia warrants an outsized credit allocation

In our view, there is a deep A$500 billion market opportunity that warrants a reallocation out of real estate equity (where we see entrenched underperformance for core strategies) and out of global credit (given more elevated risks of disruptive pricing adjustments in Europe, North America and Asia).

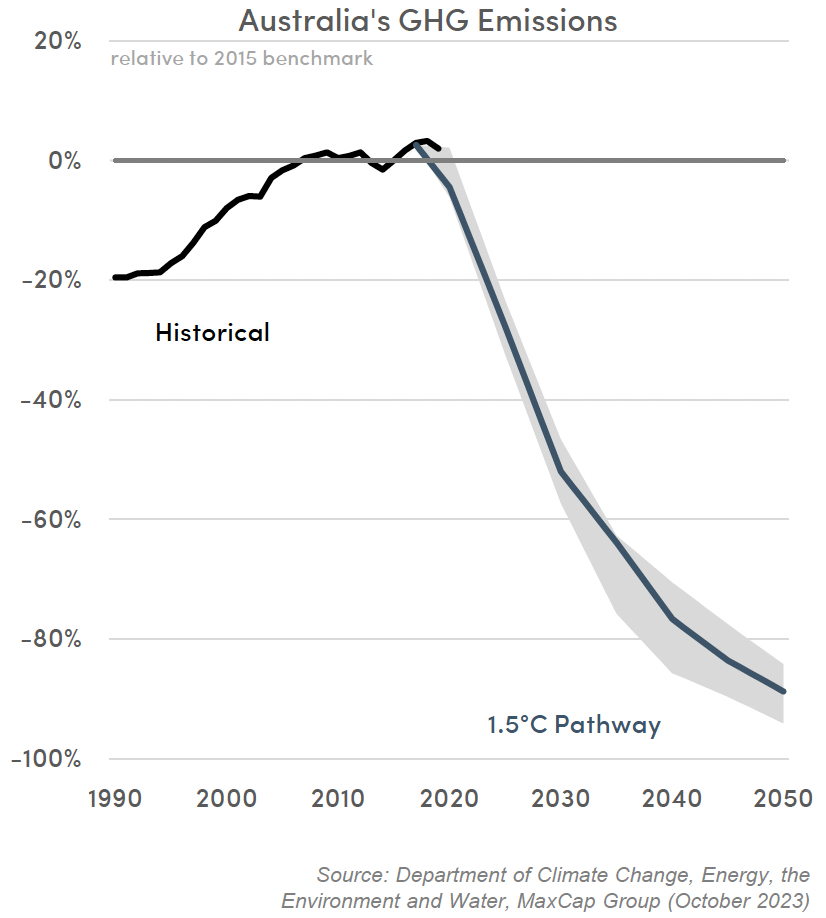

Journey to Net Zero

Confronted with more signs of climate change and more popular support for climate action, the Australian Government has committed to markedly reduce greenhouse gas emissions by 2030, on the way to net zero emissions by 2050.

A lot of real work ahead

In this context, there is a lot of work to be done in real estate, as a major emitter of carbon in the economy. Also, there is considerable opportunity ahead across Australian real estate sectors to reduce energy usage, build more sustainably, manage climate risks and deliver better risk-adjusted returns.

Covering all types of real estate

The green push in real estate is all encompassing, not just including all future construction projects, but also covering the comprehensive retrofits of every existing residential and commercial building to align with the proposed net zero pathway.

Delivering measurable outcomes

Part of this journey involves measuring the environmental performance for each asset, by continually reporting upon their sustainability ratings, as a baseline for assessing future improvements.

A green premium

For investors, there is increasing evidence of a green premium in real estate, with more sustainable buildings commanding higher occupancy, rents and asset prices. Investors are not just deploying to sustainable real estate for better environmental and social impacts, but likely for better financial rewards as well.

The great standing

Importantly, there is an element of investor value protection at work as well. For buildings left behind by the rising tide of sustainability, there is a genuine risk that browner buildings might become stranded, unable to attract finance, insurance or buyers.

A widening gap

A challenging global economy, rising interest rates and falling asset values are prompting greater caution from buyers and lenders alike. Altogether, this is creating a $5 billion real estate capital funding shortfall by diluting equity and reducing the availability of debt.

A transfer of leverage

As interest rates stay higher for longer, there are related shifts in investor focus, negotiating power and potential returns. Credit returns are lifting with higher rates and wider margins, alongside greater debt demand and weaker lender competition.

Abrupt sector rotation

Changing fortunes in real estate sectors are impacting finance availability. Banks are visibly shifting their loan allocations, reducing their relative exposure to retail initially and office more recently, amid a long running structural move from residential and land development, exacerbating the funding shortfall in these sectors.

Being selective on equity

Existing investors remain cautious overall, given the ongoing correction in asset prices. New buyers have a good bottom‑of‑the‑cycle entry window ahead, although it is important to be selective about sectors and the entry price points.

A focus on private credit

A focus on private credit. The shortage of credit puts lenders at a strong advantage, at a time of improving returns and relatively resilient incomes, especially compared to other asset classes. The credit squeeze is similarly more acute for specific sectors, even as equity investors start to return with more palatable pricing.

A time for non bank lenders

Deposit‑taking lenders are facing more constraints ahead, impacted by the fallout from the US regional banking crisis, tighter lending standards and more prudent regulators, offering considerable scope for non‑bank lending growth.