Surging tertiary enrolments

Australia remains one of the most popular destinations in the world for tertiary students. The number of international enrolments neared a million students in 2023. Given recent inflows, Australia is well positioned to exceed that mark in 2024.

Stellar student housing demand

This accelerating pace of student inflows is adding significantly to housing demand, particularly for purpose-built student accommodation (PBSA) facilities within major capital cities and around top-tier tertiary education hubs.

Not enough supply

In the face of this relentless demand, the pace of student housing supply is lagging clearly, curtailed by tough competition from other residential developers, strict planning constraints and the small number of operating partners in this sector.

Living your best life

With robust demographic tailwinds in Australia, and lingering challenges for many commercial sectors, the living sector is shaping up as a very attractive destination for investor capital for this cycle, with student housing sitting squarely in this frame.

A better yield for living

Compared to build-to-sell and build-to-rent strategies, student accommodation in Australia is delivering relatively stronger and more resilient income yields, while drawing on the same buoyant structural drivers as the broader living sector.

Greater regulatory focus

While student numbers may change for cyclical or policy reasons in 2025, the persistent undersupply of suitable housing remains in place. Policymakers continue to see additional student accommodation supply as a key part of the solution.

Packing your bags again

With the unprecedented lockdowns and re-openings of recent years, we have seen two dramatic shifts in population out of, and back into, the major capital cities. These are driving some remarkable trends in housing demand, rents and pricing.

Doing a big U-turn

The COVID years were marked initially back a hurried flight from densely-populated cities, in search of a socially-distanced lifestyle. Since then, there has been a massive population rebound within cities, partly accelerated by a renewed migration boom.

A broader uplift in rents

Amid a lack of available housing and a broad surge in rents, there is a widening performance gap taking hold, with city-centre and inner-urban rents rising more strongly, as tenants compete for a finite pool of housing closer to the central city cores.

Pricing patterns are clearly shifting

The pricing uplift of 2021 was clearly led by a range of lifestyle markets in the bush or by the beach. That pattern is unwinding with the return to work and living in the city. Inner-city markets have more scope to rise, given relentless demand.

Finding the next hotspots

We can identify forthcoming hotspots given the local patterns of housing demand and supply. Through this lens, we see more urgent undersupply in the major capital cities, and some oversupply risks in select sea-change and tree-change markets.

Follow the people (and their money)

Out of these dramatic shifts, there are clear tactical investor choices ahead. There is a broad pattern of housing undersupply that will take some years to unwind, with key hotspots likely around specific parts of major capital cities.

Revisiting the outlook

The health of the Australian construction sector remains a key area of focus for both equity and credit investors. In this report, we take a timely review of the sector outlook, noting the recent trends in costs, profitability and the degree of financial distress.

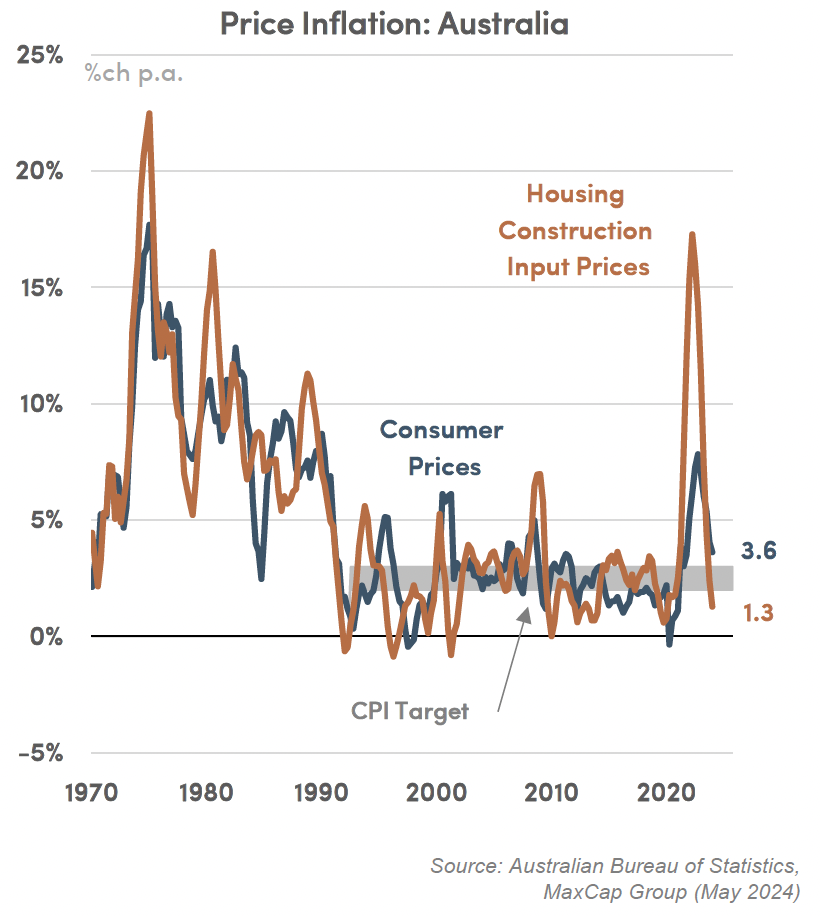

Past peak inflation

The worst price shock since the 1970s looks to be behind us, as construction cost inflation slows sharply. Building costs are finding their peak and may fall outright. This is only a partial unwind, but it does provide much-needed relief for stressed builders.

Sunnier days ahead

Indeed, the adverse profit drivers of recent years are now unwinding, particularly as construction costs stabilise, final selling prices rise, interest rates approach a cyclical peak, and we move back to sunnier weather in the more populated parts of Australia.

A more profitable vintage

In this context, we are expecting a distinctive shift in construction profitability, as builders move on from the loss-making projects from 2022, into what is shaping up to be a progressively more profitable set of projects in 2024 and beyond.

Diminishing builder distress

Meanwhile, the profit squeeze of recent years has driven more builders into insolvency. As these profit drivers improve, we expect construction insolvencies to slowly decline from here, even in the face of a broader economic slowdown in 2024.

Implication for investors

From a credit perspective, there is still a lot of work to do, even as cyclical conditions improve, to keep an eagle eye on builder / developer performance, particularly in terms of their cost management, project profitability and capacity for loan servicing.

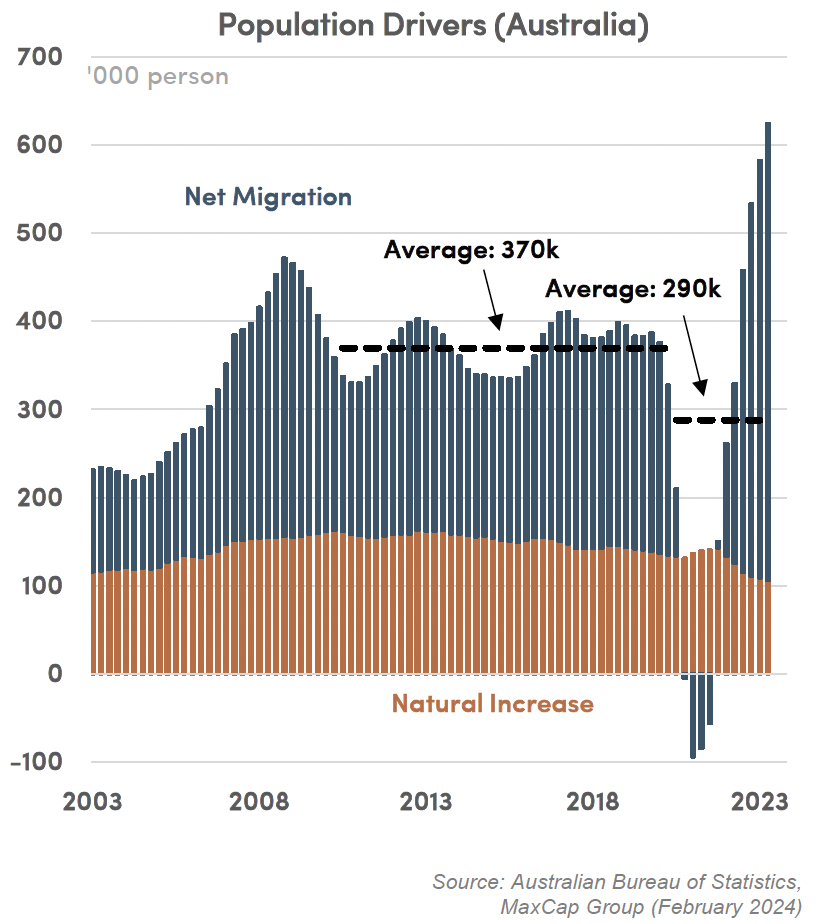

Record inflows in migration

A decade-long surge in net overseas migration is driving a massive uplift in population growth in Australia. While the record pace of immigration post-pandemic might slow for policy reasons, the big impacts on housing demand are here to stay.

Demand exceeds supply

The increase in housing demand has occurred with diminished supply gains. Supply has been slowed by elevated mortgage rates, higher construction costs and wet weather. Australia is set for marked housing undersupply for some years ahead.

Acting your age

The evolving age profile in Australia is clearly shifting housing requirements as well, adding demand broadly to all types of living sectors, but also across specific age groups, including senior retirees, first home buyers, upgraders and university students.

A home among the gum trees

New arrivals from different parts of the world bring with them very different housing preferences. Indeed, migration patterns are likely to add demand concurrently for higher-density apartments, house and land packages and student housing.

Putting a roof over everyone

With this firm pace of housing demand, there are more urgent calls to lift housing supply, via a policy push for speedier and friendlier development approvals. However, this catch up in supply will likely take several years to unfold nationwide.

Firm performance drivers ahead

Persistent housing undersupply is pushing residential vacancies to ultra low levels, unleashing a sizeable surge in rents. Growing residential rents are offering a strong hedge against inflation, especially compared to lagging commercial rents.