An evolving landscape

The investment market landscape is looking more challenging again in 2025 as a global trade war threatens the outlook with softening economic growth, rising price inflation and elevated uncertainty. Consistent returns are getting harder to find.

On credit selection

Institutional investors are looking broadly across credit markets – public and private, here and abroad – to find suitable exposures, at a time of increased volatility and decreased transparency in global equity markets, but credit selection is not easy.

Perusing the menu

There are numerous options across credit markets, which offer vastly different risks and returns exposures. That said, historical returns have been modest across a range of public credit market benchmarks, given periodic and sizeable drawdowns.

Making the grade

Within specific credit market segments, there are more nuanced choices up and down a familiar risk return curve. In this context, we can position segments like commercial real estate debt, which has historically offered consistent returns, with low volatility.

Seeking diversification

Meanwhile, we have seen a concerning lack of diversification across different asset classes, following correlated dips in equity and credit returns in 2022 and potentially again in 2025. For now, commercial real estate debt returns remain lowly correlated.

Taking credit where credit is due

In a challenging world with elevated uncertainty, diminishing growth and volatile returns, there is a keen push to support portfolio returns and improve diversification, with private credit well positioned to deliver on both fronts.

A looming global storm

In an uncertain market landscape, an unfolding trade war is impacting heavily on the outlook, potentially pushing the global economy into recession in the near term, and permanently reshaping trade and capital flows over the longer term.

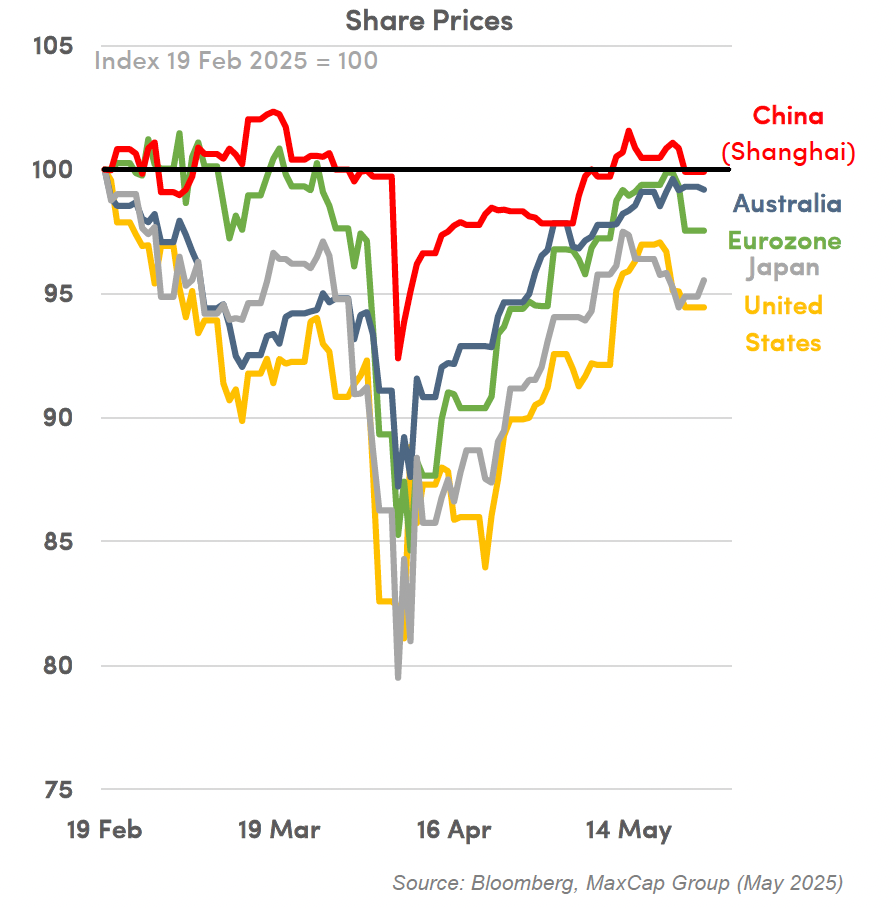

Fright and flight

Capital markets around the world have reacted abruptly to this outlook, with sharp pullbacks in share and bond prices, along with big jumps in market volatility. There is nuance in this market, with some regions (like the US) being more harshly affected.

Bracing for impact

As with prior cycles, offshore shocks will have local impacts. Higher US tariffs will slow export demand for both China and Australia. Arguably, the larger impacts will come through financial channels, given reduced wealth and diminished confidence.

Timely shock absorbers

In previous downturns, there were well‑honed shock absorbers at work in Australia. Lower rates would boost domestic sectors. A weaker currency would provide a competitiveness boost for exporters. Most of these shock absorbers are at work again.

Finding a harbour in rough seas

For investors, the lack of portfolio diversification is particularly concerning. In 2025, much like 2022, the traditional mix of stocks and bonds is not providing adequate portfolio stability. Investors need to look elsewhere for shelter in a rough storm.

Finding your way

More than ever, investors are looking more broadly to rebuild diversification and sustain returns. Portfolios are reallocating from public to private markets and from equity to debt exposures. Private credit remains well placed to offer that resilience.

Now for the downhill run

After the most aggressive interest rate tightening cycle in modern history, we are finally moving past the peak. More central banks are now easing to stimulate their economies, with Australia finally joining the rate-cutting bandwagon in early 2025.

A small step for rates, a giant step for sentiment

As the economy moves to modestly lower rates, we expect to see a bigger shift in sentiment, with significant implications for the most rate-sensitive sectors, particularly consumer spending and housing construction.

Better construction feasibility

The building sector, long constrained by high material and borrowing costs, is set for a stronger outlook in 2025. Slower cost inflation and lower funding costs ahead should drive a clear turning point and rebound in building activity from here.

Some relief on affordability

For home buyers, higher mortgage rates have been a prominent factor behind the debilitating squeeze on housing affordability. Mortgage rates are falling in 2025, which should provide much-needed relief for financially-strained households.

What are the implications for credit?

We see modestly lower rates in 2025 as a better sweet spot for private credit. While floating-rate interest repayments may edge slightly lower, we expect to see some offset from stronger borrower appetite and increased lending volumes.

Strategies for changing rates

For many asset classes, changes to the growth or rate regimes may drive big changes to the returns outlook. For commercial real estate debt, these regime changes are less relevant, given a long historical track record of stable returns.

Turn in, apex and exit

Since 2020, real estate markets have seen some interesting times, as supply chain disruptions, cost inflation and higher rates all combined to weigh down asset prices. In 2024, the downturn has run its course, as we look forward to the next upswing.

Eyeing the corner

Heading into 2025, there are more definitive signs of a turning point in local commercial real estate markets, marked by stronger share prices, firmer investor sentiment and a cautious uplift in transactions, even ahead of actual reductions in policy interest rates.

Foot on the accelerator

Already, we are seeing gains in commercial asset values for the first time this cycle. While these initial price gains are modest, they do signal a clear change in sentiment as investors move from fear to greed, from loss aversion to a search for profits.

A model’s outlook

We can use simple econometric models to illustrate the potential impacts of firmer market conditions, to better understand the timeframes for a turnaround and the likely extent of the subsequent rebound in prices or recompression in cap rates.

Compression and ignition

With an improving real estate market, we anticipate a broadening recovery to come through as firmer cap rates in 2025. The initial pace of cap rate recompression is likely to be quite modest, as it will take some time for markets to gather momentum.

Strategies for the next lap

As investors look for a timely window for a return to market, it is important to reinforce the perennial importance of sector selection in 2025. The outlook remains strong for living sectors, as out-of-favour sectors make a slower comeback.