As cloudy as ever

As any veteran forecaster will tell you, the crystal ball is as cloudy as ever. Trade discord continues to weigh heavily on the global outlook. To this, we now add stretched valuations for US technology stocks, driven by buoyant expectations for artificial intelligence.

Sluggish growth, high inflation

In 2026, major economies are facing mild stagflation – sub-par growth and elevated inflation. Population growth remains firmer in Australia and more subdued in New Zealand, driving divergent demand cycles in 2026 and beyond.

The end is nigh for rate cuts

Stubbornly elevated inflation will bind the hands of central bankers. The window for rate cuts has closed. Investors are now turning their attention to rate hikes in 2026. Investors need to reconfigure their portfolios for this new economic landscape.

““The outlook for 2026 presents a lot of noise for investors to deal with. The key, as always, is to find the signal and identify the investment opportunities with sound risk adjusted returns. At MaxCap, we are keenly focused on sourcing high-quality opportunities in segments with strong demand fundamentals – clearly evident right now in the living and logistics sectors. With our established borrower relationships and disciplined approach to origination, we are well positioned to navigate this competitive lending landscape and deliver consistent returns for our investors.” “

Executive Chairman

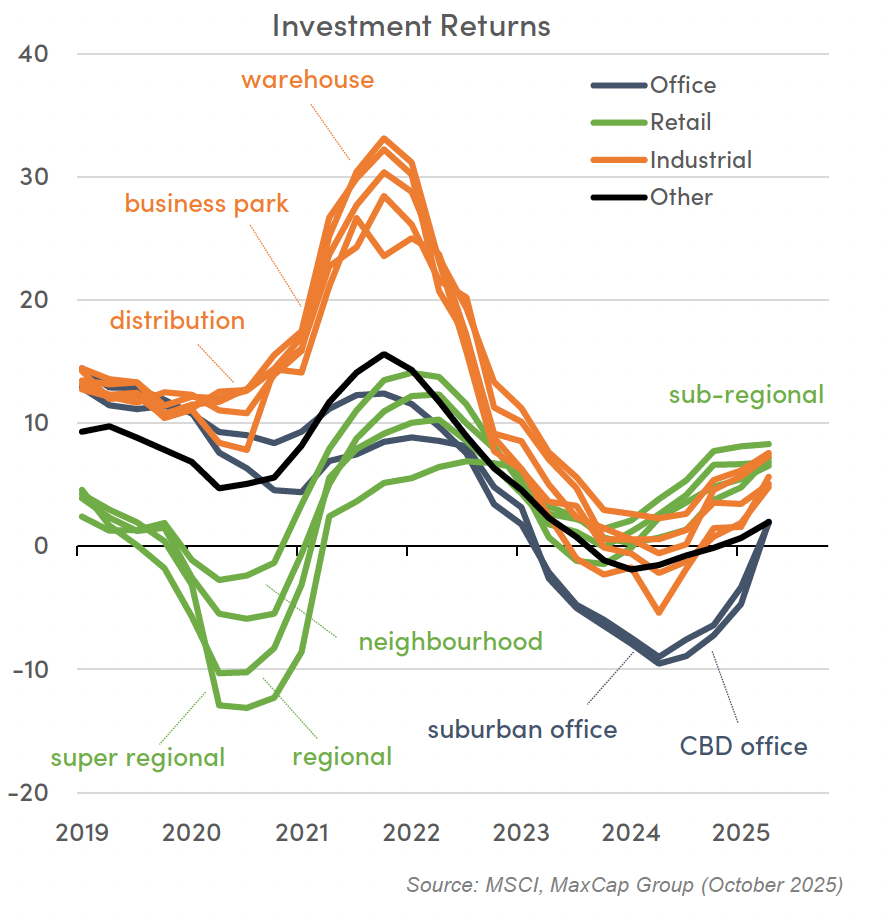

Credit versus equity

Interest rates set the price of money over time. It also tilts the balance between equity and credit returns. At current rates, real estate credit is still outperforming real estate equity, albeit to a narrower extent, as equity rebounds in 2026.

Sector selection

While more sectors are returning to profitability, there is likely to be persistent alpha from sector selection. Residential and living segments are still well set to lead the way, followed by industrial and retail sectors, with office expected to lag in 2026.

Navigating markets in 2026

With a subdued economic outlook, investors are set to push into real, resilient incomes, particularly where there are good demand fundamentals like the living sector. The need for inflation and rate hedges are bringing the focus back onto real estate.

““While macro setting remains volatile, we’re seeing borrowers increasingly gravitate to market players who have a strong track record to provide certainty when it comes to funding requirements. This trend will continue throughout 2026.””

Executive Director

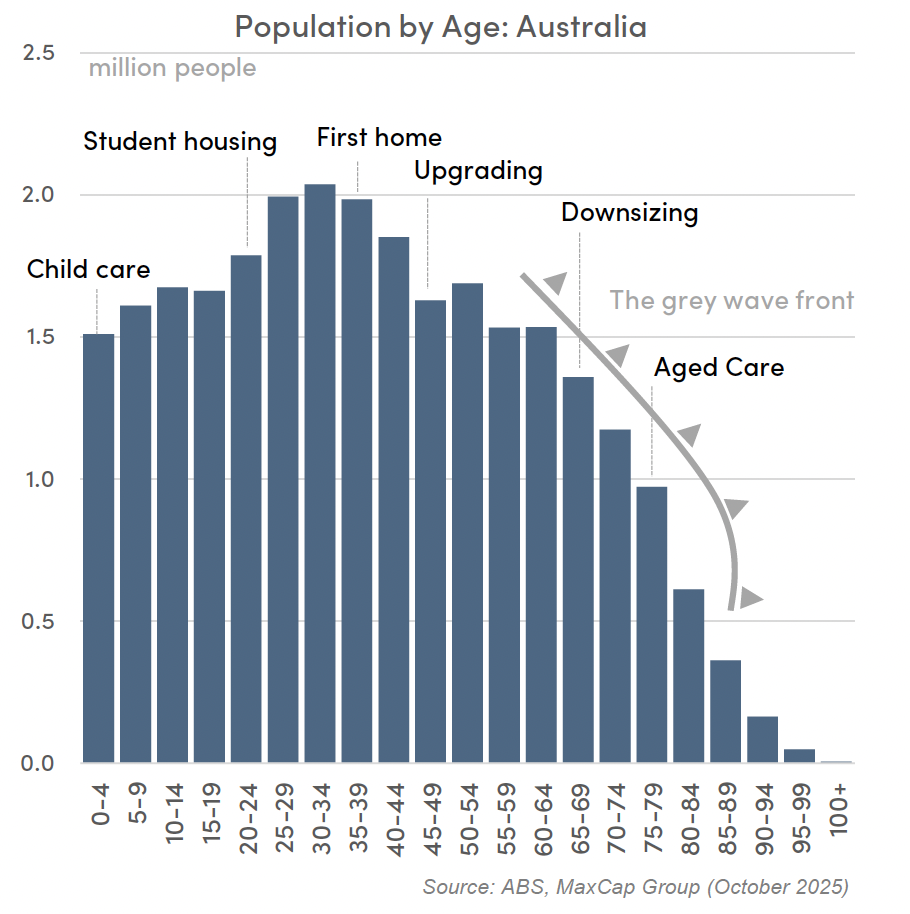

Demography is destiny

Changes to the population profile have big implications on the pattern of housing demand. Indeed, Australia’s population growth is driving strong demand for student housing, affordable first homes, downsized apartments and senior living.

They grey wave

What is particularly interesting is the move by impending retirees in their 50s and 60s from large empty-nester houses into smaller and more suitable apartments. Population ageing will drive a big downsizer movement over the coming years.

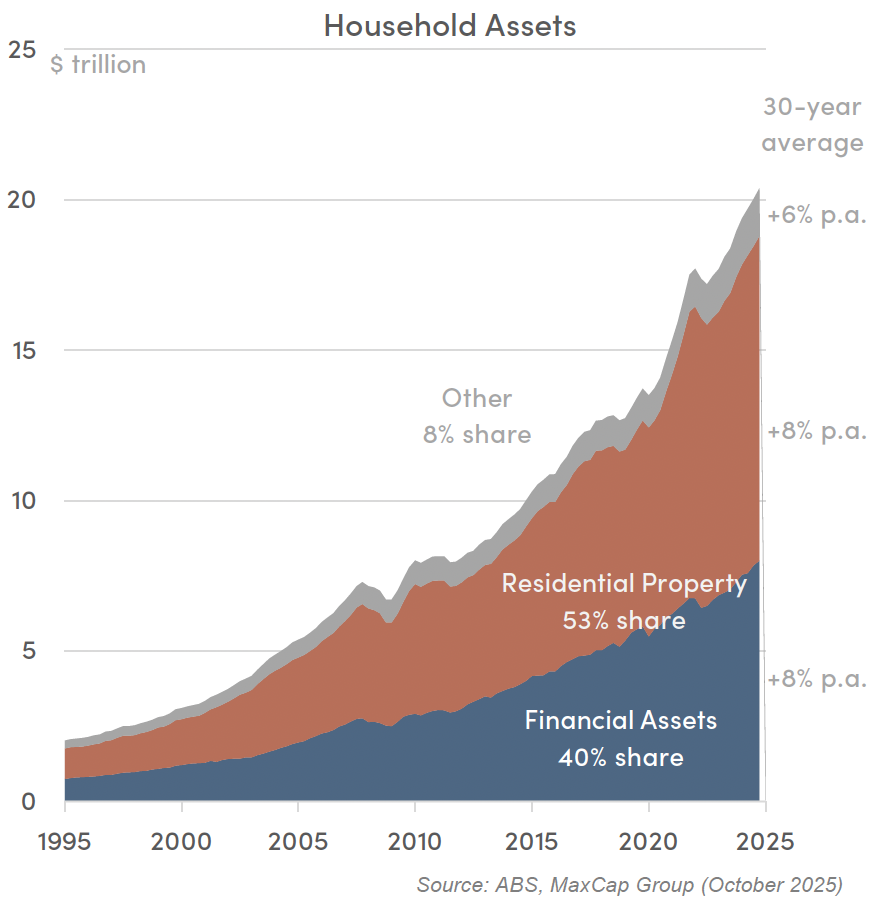

Unlocking real wealth

The downsizing movement is partly driven by lifestyle reasons, but also by strong financial incentives. For many households, their home is their biggest asset, and their biggest source of wealth creation. For many, retirement is a prime liquidity window.

Downsizing for dollars

In moving from larger houses to smaller apartments, even in a similar location, households can unlock sizeable pools of equity from their long-held illiquid asset. This price gap is particularly large in major capital cities like Sydney.

The upmarket downsizers

The sharp end of this adjustment is much narrower in scope, with a keen focus on older, wealthier suburbs, where there is a more substantial price gap (and arbitrage opportunity) between older, larger houses and smaller, amenity-laden apartments.

The real opportunity ahead

For real estate developers, there are specific buyer preferences to keep in mind. Location is vital – it is important to be near to existing family and friends. Product is key – given an increased focus on quality, amenity and accessibility.

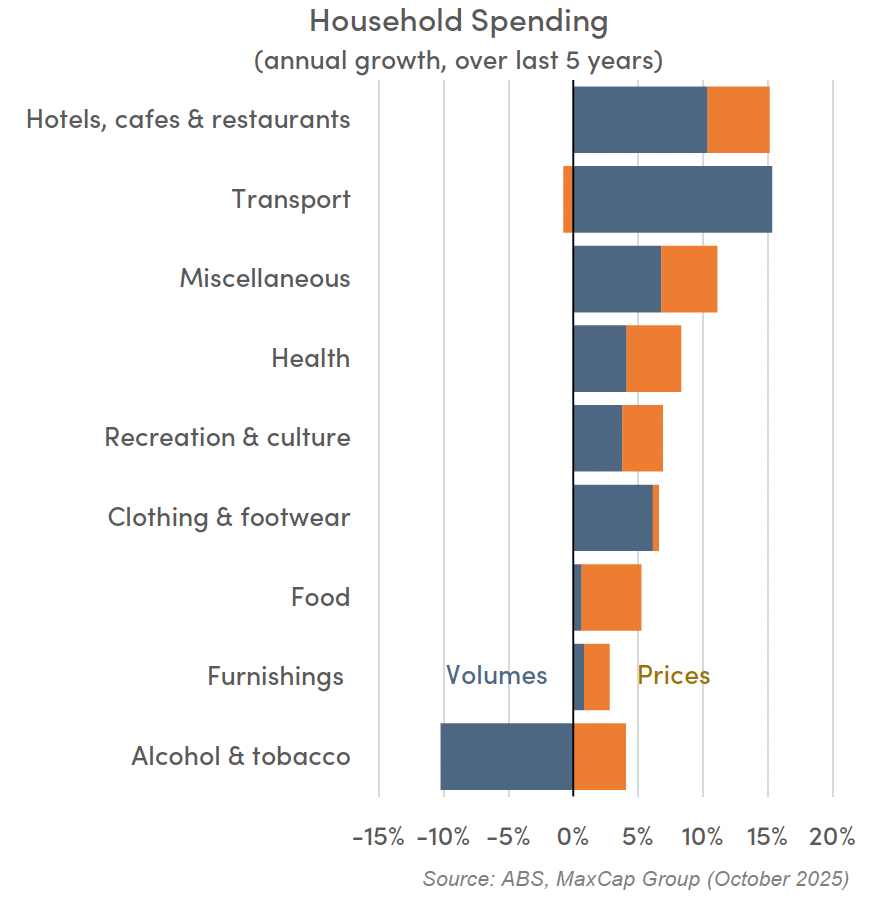

Shoppers unshackled

After several challenging years, households are gradually returning to retail spending, unshackled by lower interest rates and lower mortgage repayments. The uncertain global outlook is not hitting local sentiment in the same way, as we are seeing abroad.

A different shopping basket

The returning shopper looks very different in 2025. After a lockdown, there is a clear reset in priorities. There is a sense of revenge shopping, to make up for lost time, as spending skews towards dining out, travel and personal services.

Finding a new equilibrium

Meanwhile, the big structural headwinds for the retail sector are gradually subsiding. Households are not rushing to online portals with the same fervour, as in‑store sales recover, and more people find a new balance to their shopping habits.

Remixing tenants

In the face of changing consumer behaviour and online shopping, retail landlords are adapting accordingly. There is an urgent push to remix tenancies within shopping malls, incrementally shifting towards dining, personal services and experiential offerings.

A shopping mall comeback

Certainly, the retail sector has seen a long correction since 2018, more so in regional and sub‑regional malls, and less so in resilient large‑format centres. In 2025, there is a broader recovery taking hold, driving higher rents and firmer yields.

Retail outperformance

For now, retail shopping centres are outperforming office and industrial, given their relatively greater sensitivity to lower interest rates. The gap between equity and credit returns is narrowing, with lower cash rates being the key catalyst.

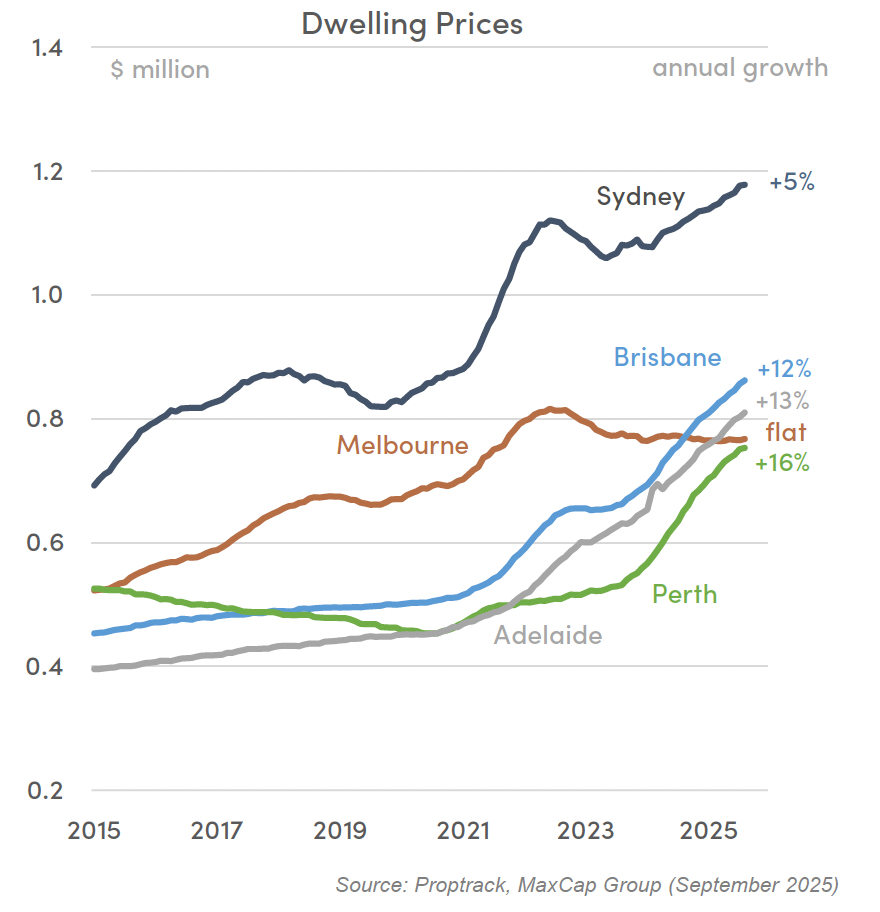

Melbourne residential underperforms

The Melbourne housing market has noticeably underperformed since 2022, with a modest local price correction in recent years, compared to the sustained pricing uplift observed in most other capital city markets in Australia.

A heavier tax burden

There are many reasons behind this subdued performance. The need to repair the Victoria state budget has drawn a broad suite of local property taxes. In turn, investors have been badly spooked by this higher tax burden and reallocated elsewhere.

Sustained housing demand

Housing market fundamentals remain favourable for Victoria. Demand is still being buoyed by firm overseas migration and diminishing interstate outflows. When set against the subdued construction pipeline, Melbourne remains well undersupplied.

Lower rates as the catalyst

With the move to lower interest rates in 2025, the housing market is set for another cyclical upturn. Melbourne is well positioned for this upswing, given relatively more affordable price points, especially compared to other, more expensive markets.

The road to recovery

After a long run of underperformance, Melbourne residential is finally set for a pricing recovery in late 2025 and 2026. To be clear, Melbourne’s price discount is likely to persist, rather than narrow over the course of the next upswing.

Navigating the comeback

For developers who have been downbeat about the prospects for Melbourne, we are expecting a cyclical turning point to take hold. Lower borrowing costs and higher selling prices should be key factors behind a cyclical uplift in building activity ahead.